ADAM LERNER

Principal/Sr. Director, Research – Global Equities

The long-anticipated June 12th SpaceX IPO is expected to raise $75 billion, more than double the near $30 billion that Saudi Aramco raised when first listed in 2019. The initial $1.77 trillion target valuation for SpaceX would immediately rank it among the world’s 10 largest companies, comparable to the likes of Broadcom and TSMC. There are also two hotly anticipated IPOs in the AI space. At the start of June, Claude AI creator Anthropic filed for an IPO, and OpenAI followed suit one week later. Market speculation suggests that both companies may go public before the end of the year, with IPO capital raises exceeding $50 billion each and valuations approaching $1 trillion.

The upcoming additions of SpaceX, Anthropic, and OpenAI to the universe of public equities will meaningfully reshape global benchmarks over the long term and likely impact market liquidity and volatility. The combined estimated valuation of $3-4 trillion for these three IPOs alone is equivalent to just over 5% of the S&P 500 market capitalization as of May month-end. Further, there are other notable IPOs expected in the near future—such as ByteDance, Databricks, and Stripe—that could further reshuffle the public equity landscape.

In this piece, we explore the implications of the market impact of the forthcoming megacap IPOs, how index providers have been preparing for these additions, considerations investors should weigh for their portfolios, and historical precedent for megacap IPO performance.

Market Impact of Upcoming IPOs

Historically low free float percentages in the mid-single digits for these megacap IPOs should dampen the immediate impact on indices. As opposed to a more traditional 90- to 180-day IPO lockup for insiders, SpaceX has established a staggered release over the next six months that will allow most insiders (Elon Musk has agreed to a 366 day lockup) to sell shares early and has the potential to increase tradeable float faster. As lockups expire and more shares become available, SpaceX and the other IPOs will increasingly become sizable market constituents.

- Stock Weights: As of the end of May 2026, there were only seven companies in the global MSCI ACWI Index with float-adjusted market caps exceeding $1.77 trillion, the target valuation for SpaceX. While that dollar level would equate to a benchmark weight of close to 1.7%, we note that the actual initial sub-10 bps weight reflects initial free float below 5%. Based on target valuations of close to $1 trillion, Anthropic and OpenAI may also rank among the 20 largest public companies following their IPOs.

- Sector Weights: While SpaceX will be classified under Industrials, many upcoming IPOs, including Anthropic and OpenAI, will be classified under Information Technology. Led by NVIDIA, Apple, and Microsoft—which combined account for 12%+ of MSCI ACWI Index assets as of the end of May 2026—the near one-third level of index assets classified as Information Technology should increase in coming years.

- Forced Selling of Existing Constituents: The introduction of megacaps to indices will require proportional reductions of remaining positions. While low free float levels for upcoming IPOs should not have a meaningful liquidity impact at first, we would expect the individual weights of current market leaders to shrink over time to accommodate the increased number of companies with outsized valuations.

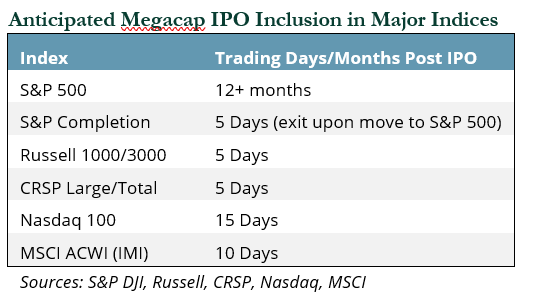

Rules for Megacap IPO Inclusion

A number of index providers recently reevaluated their methodology in advance of the upcoming IPOs. FTSE Russell, following its recent consultation, reported that it revised previous rules requiring companies to wait for the next annual index review before they could be included. As a result, megacap companies like SpaceX can now enter indices after five days of public trading. Nasdaq reported that it also recently adjusted its rules to allow for entry after 15 days, using an adjusted free float that will lead to a higher weighting than peers. MSCI and CRSP have historically allowed for faster entry of IPOs into major indices, and both have indicated that this approach will not change.

S&P 500 Index Stands Pat

S&P Dow Jones Indices (“S&P DJI”) announced in early June that no changes will be made to the existing seasoning period, financial viability, or minimum free float criteria for megacaps in its flagship S&P 500 Index. S&P DJI reported that it considered narrowing the window for inclusion from a current minimum of 12 months, subject to both positive net income across the four most recent quarters on a GAAP basis and a minimum 10% free float requirement, to as soon as six months while waiving requirements. While proponents of the existing rules emphasized that maintaining them could help avoid forced buying of unprofitable and illiquid stocks, advocates for fast inclusion stressed their belief that indices should include megacap stocks in the investable universe.

Through the end of 2024, S&P DJI estimated that just over $20 trillion in assets were benchmarked to the S&P 500 Index, with close to two-thirds of that total in passively managed assets. Data from Bloomberg Intelligence suggests that the delay in including SpaceX in the S&P 500 Index could initially reduce forced buying by close to $14 billion, a total potentially matched by combined levels for Anthropic and OpenAI later this year.

In our view, passive investing trends suggest that, even with the decision by S&P DJI, the upcoming IPOs will lead to meaningful buying activity across index providers. Morningstar Direct data as of the end of 2025 indicates that there is $19+ trillion in passively managed funds, representing over 55% of net assets as investors continue to gradually move from active to passive investing. Across U.S. equity funds, where most of these upcoming IPOs will be introduced, active management accounted for less than 35% of category assets. The growing trend of risk-aware equity products could further drive forced purchases of IPOs.

Portfolio Construction Considerations

We anticipate that SpaceX and subsequent megacap IPOs will be included in the MSCI ACWI indices 10 trading days post-IPO. These global equity indices serve as the benchmark for many investors’ public equity segments. Delayed allocations to the megacap IPOs as a result of index provider or active manager selection could lead to moderately higher tracking error across public equities. While we don’t believe that the initial sub-10 bps weight for SpaceX in the MSCI indices should be a material driver of segment relative performance, further increases in weight before client adoption—or the introduction of multiple megacap IPOs within a short timeframe—could be more impactful.

With CRSP and FTSE Russell both likely introducing IPOs after five trading days, and NASDAQ opting for 15 days, those index providers should incorporate megacap exposure into their all and large cap products more quickly.

The notable exception is funds benchmarked against the S&P 500 Index. With the recent decision by S&P DJI to maintain existing rules that will preclude inclusion of megacap IPOs in its flagship index for at least a year, the meaningful delay in timing versus other providers has gained investors’ attention. Investors in S&P 500 benchmark funds that want more immediate megacap IPO exposure within the domestic large cap segment could consider comparable low-cost passive funds managed against the CRSP Large Cap Index (or secondarily the Russell 1000 Index).

For investors opting to maintain passive exposure through the S&P 500 Index, one option is to consider investing in a fund benchmarked to the S&P Completion Index. We note that, while this has traditionally been a small-mid cap index, it includes all stocks in the S&P Total Market Index that are not yet represented in the S&P 500 Index. Recent methodology adjustments by S&P DJI to allow inclusion of stocks in these indices with float-adjusted market cap greater than 10% of the 100th largest company in the S&P Total Market Index will result in SpaceX, and subsequently Anthropic and OpenAI, being included in the index five trading days post-IPO until ‘graduating’ to the S&P 500 Index. Initial indications suggest SpaceX may enter this benchmark in June as a top five holding with an initial weight near 1.0%.

Short-Term Performance of IPOs

Recognizing the year-plus lag before SpaceX, Anthropic, and OpenAI enter the S&P 500 Index raises the question of how IPOs have historically performed following their initial public offerings.

While past performance may not be indicative of future results, the five largest U.S. IPOs by initial market cap valuation posted significant losses 12 months later, with an average decline of almost 40%.

Other highly anticipated IPOs in recent decades, including Snap and General Motors, experienced one-year losses exceeding one-quarter of their initial value. Data from 1980 through 2024 compiled by Jay Ritter, Director of the IPO Initiative at the University of Florida[1], indicated that U.S. IPOs, on average, lagged companies of similar size and valuation by 280 bps one year after listing, with underperformance persisting for five years.

Time will tell how upcoming IPOs perform, although we are mindful that frenzied excitement for the launches (the SpaceX IPO is two times oversubscribed), historically low initial free floats (SpaceX is sub 5% with single-digit levels expected for Anthropic and OpenAI), and the current bull market could all be contributing to what may be lofty initial prices.

Final Thoughts

While IPOs are not a new phenomenon, we believe that the expected valuations for the upcoming SpaceX, Anthropic, and OpenAI launches could have an unprecedented impact on market composition and subsequently index composition as free float broadens. It will lead to forced selling of existing investments across both passive and risk-aware products, with the magnitude of the impact driven by factors including evolving float percentages for IPOs and timing of companies going public.

The three headline IPOs set to launch in coming months will likely be followed by others as demand warrants. Benchmarking and passive index fund selection become increasingly important in this environment, particularly when considering the divergence between how quickly these new equities will be included in the various large cap indices.

While we recognize the market fervor that has generated strong initial demand for exposure to these innovative companies, history suggests that the strong returns generated for private equity investors may not carry over to public equity markets in the short term.

[1] Initial Public Offerings: Long Run Statistics, Jay Ritter, Warrington College of Business, University of Florida. https://site.warrington.ufl.edu/ritter/files/IPOs-long-run-returns-on-IPOs.pdf

Indices referenced are unmanaged and cannot be invested in directly. Index returns do not reflect any investment management fees or transaction expenses. Copyright MSCI 2026. Unpublished. All Rights Reserved. This information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an “as is” basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any other person involved in or related to compiling, computing or creating this information makes any express or implied warranties or representations with respect to such information or the results to be obtained by the use thereof, and MSCI, its affiliates and each such other person hereby expressly disclaim all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any other person involved in or related to compiling, computing or creating this information have any liability for any direct, indirect, special, incidental, punitive, consequential or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have anticipated, the possibility of such damages. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and / or Russell ratings or underlying data and no party may rely on any Russell Indexes and / or Russell ratings and / or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. Copyright ©2026, S&P Global Market Intelligence (and its affiliates, as applicable). Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collecti Indices. Bloomberg does not approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, it shall not have any liability or responsibility for injury or damages arising in connection therewith. All commentary contained within is the opinion of Prime Buchholz and is intended for informational purposes only; it does not constitute an offer, nor does it invite anyone to make an offer, to buy or sell securities. The content of this report is current as of the date indicated and is subject to change without notice. It does not take into account the specific investment objectives, financial situations, or needs of individual or institutional investors. Information obtained from third-party sources is believed to be reliable; however, the accuracy of the data is not guaranteed and may not have been independently verified. Performance returns are provided by third-party data sources. Past performance is not an indication of future results. Some statements in this report that are not historical facts are forward-looking statements based on current expectations of future events and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. Nothing herein should be construed as a guarantee of future results. © 2026 Prime Buchholz LLC