BY JESSE LYNCH

Principal/Sr. Director, Research – Real Assets

Summary

The war in Iran has caused a historic supply shock to global energy markets. At the center of the disruption is the Strait of Hormuz, a narrow but critically important waterway through which a meaningful share of global oil, seaborne liquefied natural gas, and other essential commodities typically flow.

The issue is not simply the volume of oil and natural gas that pass through the strait, but the concentration risk it represents. The waterway is a key export route for major Middle Eastern oil producers, regional food flows, and a conduit for the global fertilizer trade. An extended disruption can expand beyond oil and gas into the broader inflation and growth outlook.

Market moves to date reflect this uncertainty. Crude oil, refined products, and regional natural gas spot prices have all been repriced sharply as investors and physical market participants assess the likely duration of the disruption and the extent of any damage to regional energy infrastructure.

In this investment perspective, we examine why the Strait of Hormuz matters so much, how energy markets have responded, what a prolonged disruption could mean for energy markets and the best way to protect portfolios from these types of shocks and other periods of rising resource prices.

Why Hormuz Matters

The Strait of Hormuz is a strategically important waterway in the global economy and plays an outsized role in global commodity flows. The strait carries more than 20% of daily global oil supply, roughly a quarter of seaborne natural gas (which represents a smaller portion of total global natural gas supply but is still very impactful on pricing), material volumes of global fertilizer supply, and food imports for parts of the Middle East.

That concentration is important as short-term substitutes are limited. Storage, alternate pipelines, rerouting, and strategic reserves can soften the shock, but they do not fully replace the ability to move large volumes of energy smoothly and continuously out of the region.

The duration of the disruption is the key variable. Historically geopolitical supply shocks have been relatively short-lived, with the 1970s oil embargo being an exception. A closure lasting several weeks may prove less impactful, however disruption measured in months would be more consequential, with broader implications for inflation, business confidence, and real economic activity. In that scenario, the risk of a stagflationary backdrop becomes more relevant.

Market Impact

Energy markets have already registered a significant shock. Spot Brent crude has traded roughly between $85 and $115 per barrel, up from about $71 before

the conflict. That range highlights how markets are repricing the estimated duration of supply loss (with Hormuz closed) and uncertainty around the path forward for damaged energy infrastructure and production restarts.

U.S. spot gasoline and diesel prices have risen sharply since the start of the conflict, underscoring how energy shocks can impact consumers and businesses. Those downstream effects can broaden inflationary pressure beyond headline energy categories.

Natural gas markets have been more regionally differentiated. European gas prices have risen substantially, reflecting Europe’s ongoing reliance on global LNG markets after its pivot away from Russian gas. In contrast, the U.S. natural gas market appears relatively insulated outside of areas with greater LNG dependence, such as New England. Domestic supply abundance and constrained export capacity may continue to reduce sensitivity of U.S. gas prices.

Asia appears to be facing immediate physical market stress. Oman-linked crude pricing has risen sharply, reserve releases have been announced in parts of Asia, and buyers in both Asia and Europe are seeking additional U.S. LNG cargoes.

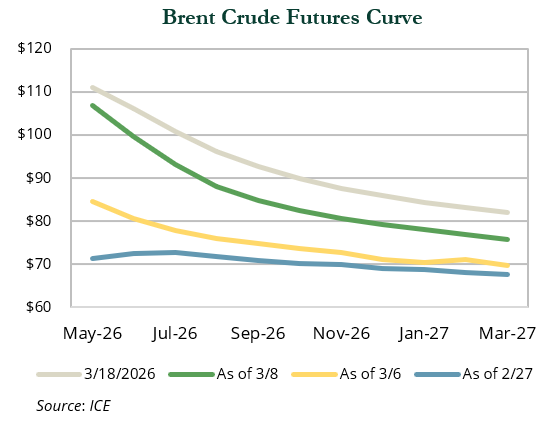

Futures Curve Reprices

One of the more important developments has been the move higher in longer-dated crude contracts. Early in a geopolitical shock, front-month volatility often dominates. When deferred contracts also move higher, it suggests markets expect the disruption and its consequences to last longer than initially assumed.

That matters because the pre-conflict backdrop was relatively benign for oil. Markets had generally expected an adequately supplied 2026 environment with crude prices in the high-$60s to low-$70s per barrel. The move away from that assumption indicates a reassessment not only of near-term supply, but also the time needed for markets to normalize. Damage to regional energy infrastructure, which has accumulated in recent periods, could reinforce that shift. Even after transit routes reopen, output may not normalize immediately if upstream or export facilities have been impaired. In addition, producers curtailing output due to transport bottlenecks may require time to ramp back up. A transit shock can therefore become a broader supply recovery issue.

Recent Events

- The U.S. and allies have initiated efforts to reopen the strait, sending attack jets over sea lanes and Apache helicopters to shoot down drones. The White House has also called on allies to send warships to help secure the strait, including Japan, China, France, the UK, and others.

- Attacks on energy infrastructure, terminals, and production assets have escalated in the most recent period. Damage to terminals and LNG facilities is being watched closely, as they can have longer repair timeframes.

- IEA announced a record 400M bbl strategic reserve release (largest in history) across 32 countries. Barrels will flow gradually over months due to physical drawdown limits.

- The U.S. also announced a 60-day Jones Act waiver to allow foreign-flagged vessels to transport oil, liquefied natural gas, fertilizer, coal, and a range of other critical commodities between U.S. ports.

- China has a massive strategic oil reserve which it has begun tapping into.

- Many Middle Eastern energy producers are reducing oil/gas production as they have no viable way to move oil out of the region, and storage is becoming an issue. Re-ramping production after an end to the conflict can take some time to execute.

- A desalination plant in Bahrain was attacked by Iran. The CIA and others have called water the most strategic commodity in the mid-east as countries in the region rely on desalination plants/related infrastructure for much of their drinking water.

Broader Portfolio Impacts?

For equities, the impact is likely to be uneven. Energy producers and select real asset exposures may benefit from stronger pricing, while energy-intensive sectors face margin pressure. The energy sector only represents 4% of assets across global indices such that continued strength during March in that sector has been more than offset by weakness elsewhere. Broader equity markets may struggle if higher energy prices begin to weigh on consumer spending, corporate confidence, or inflation expectations. The U.S. economy is not immune to such pressure, but its energy independence provides some level of insulation from a significant shock. Major economies in Europe and Asia appear particularly vulnerable to economic disruption as heavy importers of Middle Eastern energy.

For fixed income, the tension is familiar: slower growth can support bonds, but higher energy prices can reduce the scope for central bank easing. If markets begin to price a stagflationary outcome, the diversification benefit of nominal duration may prove less straightforward than in a standard growth scare. Credit markets also merit close attention, particularly in sectors sensitive to transport costs, inputs, or weakening demand.

Recent market action points to investor angst over the potential inflationary impact of the conflict and rising energy prices. Treasury yields have risen to build in a higher inflation premium, with expectations that the Fed may be less likely to reduce rates this year. Month-to-date as of March 18, most fixed income sectors are negative, with longer-term bonds suffering the most.

Gold may continue to benefit from heightened geopolitical risk and policy uncertainty, but the potential for higher rates is a headwind for the precious metal.

Key Considerations

Reopening the Strait

The single most important variable is how quickly the Strait of Hormuz reopens to non-Iranian tanker traffic. If shipping resumes in an orderly way, energy markets may begin to retrace some of the current risk premium.

Infrastructure Damage

The extent of damage to oil, gas, export, and related infrastructure is a critical secondary consideration. Even if transit routes improve, supply may remain constrained if production and processing, assets have been impaired.

Policy Response

Strategic reserve releases and efforts to secure alternative supply may help stabilize markets. Still, reserve releases flow gradually, and logistical limits won’t replace disrupted flows.

Inflation and Growth Trade-Offs

A short disruption may be absorbed as a temporary inflation impulse. A longer interruption in the strait would raise the probability that higher energy costs begin weighing more directly on growth, confidence, and policy expectations.

Portfolio Resilience

Episodes like this reinforce the value of diversified portfolio construction. Energy prices are inherently difficult to predict. In our view, a dedicated and diversified real assets allocation remains one of the best strategies to consider for navigating resource scarcity, inflation pressure, and the price shock we are currently seeing.

Concluding Thoughts

Geopolitical disruptions in energy markets have often proven shorter-lived than feared. This episode may or may not have a long-term impact, but it has the potential to be more consequential because it centers on one of the world’s most important energy chokepoints.

For investors, the key question is whether this remains a temporary shock premium or develops into a longer-duration inflation and growth event. That distinction will depend primarily on the reopening of the strait and secondarily on the extent of infrastructure damage in the region.

We will continue to monitor the market implications of this disruption across energy, broader portfolios, the macroeconomic outlook, and policy expectations. Please reach out with any questions.

All commentary contained within is the opinion of Prime Buchholz and is intended for informational purposes only; it does not constitute an offer, nor does it invite anyone to make an offer, to buy or sell securities. The content of this report is current as of the date indicated and is subject to change without notice. It does not take into account the specific investment objectives, financial situations, or needs of individual or institutional investors. Information obtained from third-party sources is believed to be reliable; however, the accuracy of the data is not guaranteed and may not have been independently verified. Performance returns are provided by third-party data sources. Some statements in this report that are not historical facts are forward-looking statements based on current expectations of future events and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. © 2025 World Gold Council. All rights reserved. World Gold Council and the Circle device are trademarks of the World Gold Council or its affiliates. The World Gold Council and its affiliates do not guarantee the accuracy or completeness of any information nor accept responsibility for any losses or damages arising directly or indirectly from the use of this information. Published LBMA Gold Price information may not be indicative of future LBMA Gold Price information or performance. None of IBA, Intercontinental Exchange, Inc. (ICE) or any third party that provides data used to administer or determine the LBMA Gold Price (data providers), or any of its or their affiliates makes any claim, prediction, warranty or representation whatsoever as to the timeliness, accuracy or completeness of LBMA Gold Price information, the results to be obtained from any use of LBMA Gold Price information, or the appropriateness or suitability of using LBMA Gold Price information for any particular purpose. to the fullest extent permitted by applicable law, all implied terms, conditions and warranties, including, without limitation, as to quality, merchantability, fitness for purpose, title or non-infringement, in relation to LBMA Gold Price information, are hereby excluded, and none of IBA, ICE or any data provider, or any of its or their affiliates will be liable in contract or tort (including negligence), for breach of statutory duty or nuisance, or under antitrust laws, for misrepresentation or otherwise, in respect of any inaccuracies, errors, omissions, delays, failures, cessations or changes (material or otherwise) in LBMA Gold Price information, or for any damage, expense or other loss (whether direct or indirect) you may suffer arising out of or in connection with LBMA Gold Price information or any reliance you may place upon it. Nothing herein should be construed as a guarantee of future results. © 2026 Prime Buchholz LLC